Managing money in today’s economy can feel overwhelming, but the 50/30/20 rule offers a straightforward roadmap for your paycheck. As of 2026, with shifting costs in housing and essential services, this classic framework remains the most effective tool for balancing your current lifestyle needs with long-term financial security.

📌 Deep Dive: Why Traditional Budgeting Isn’t Enough

Summary: While the 50/30/20 rule is a powerful framework for managing expenses, it functions within a broader economic system that often devalues cash. To make your budget truly effective, you must understand the difference between earning currency and building wealth. This video breaks down the structural “trap” of modern labor and why strategic asset allocation is the key to long-term financial freedom.

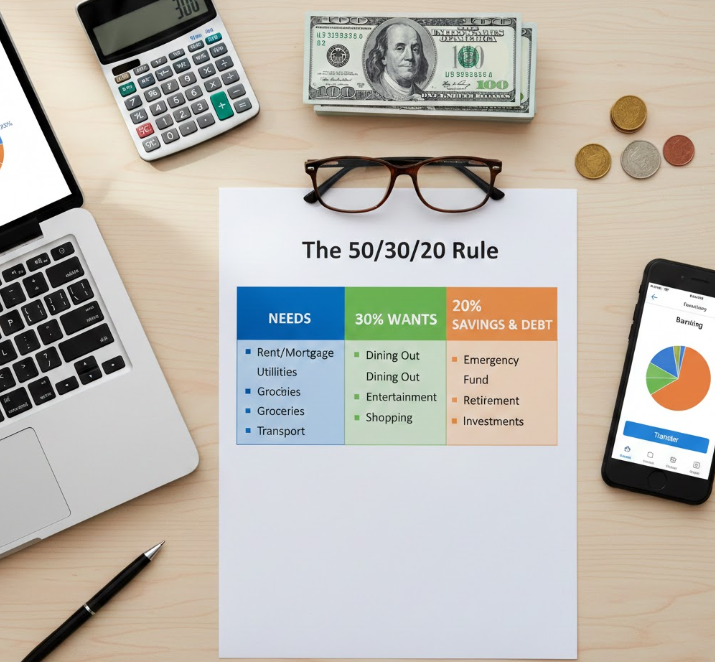

What is the 50/30/20 Rule and How Does It Work?

The 50/30/20 rule is a simple percentage-based budgeting method designed to help you manage your after-tax income. Originally popularized by Senator Elizabeth Warren, the goal is to divide your take-home pay into three specific categories: Needs, Wants, and Savings.

By using percentages rather than fixed dollar amounts, this rule stays relevant regardless of whether you live in an expensive city or a rural area. It provides a “big picture” view of your finances, ensuring that you aren’t overspending on lifestyle choices at the expense of your future security.

Before diving into percentages, make sure you have a clear picture of your current spending. You can learn how to do this in our previous guide on [how to build a simple household budget]

How Do I Calculate My 50/30/20 Budget?

To start, you must determine your “take-home pay.” This is the amount that hits your bank account after taxes and employer-sponsored health insurance are deducted. If you have automatic 401(k) contributions, you should add those back into your total income calculation to get a true sense of your 20% savings goal.

1. 50% for Needs (The Essentials)

Half of your income should be dedicated to the things you absolutely must pay to maintain your life and work. In the current 2026 market, housing and utilities often take up the largest portion of this bucket.

- Housing: Rent or mortgage payments, property taxes, and insurance.

- Utilities: Electricity, water, gas, and basic internet.

- Transportation: Car payments, fuel, insurance, or public transit passes.

- Groceries: Basic food and essential household supplies (excluding luxury dining).

2. 30% for Wants (Lifestyle Choices)

This category covers “nice-to-have” expenses. These are the costs you could theoretically eliminate if you lost your job or faced a financial emergency.

- Dining Out: Coffee shop visits, takeout, and weekend dinners.

- Subscribtions: Streaming services, gym memberships, and apps.

- Shopping: Non-essential clothing, electronics, and home decor.

- Travel: Vacation savings and weekend trips.

3. 20% for Savings and Debt Repayment

This is the most critical category for building wealth. It focuses on your future self and protecting your household from unexpected financial shocks.

- Emergency Fund: Aiming for 3 to 6 months of essential expenses.

- Retirement: Contributions to an IRA, 401(k), or other investment accounts.

- High-Interest Debt: Payments toward credit card balances or loans with high interest rates.

Comparison: The 50/30/20 Rule vs. Traditional Budgeting

| Feature | 50/30/20 Rule | Traditional Line-Item Budget |

| Effort Level | Low – Focuses on 3 main buckets | High – Tracks every single cent |

| Flexibility | High – Adjusts as income changes | Low – Often feels restrictive |

| Best For | Beginners & busy professionals | People with strict debt goals |

| Main Goal | Balance and sustainability | Absolute precision |

Is the 50/30/20 Rule Still Realistic in 2026?

A common question is whether this rule works when inflation or housing costs rise. If your “Needs” currently exceed 50%—which is common in high-cost-of-living areas—you have two primary options:

- Reduce your “Wants”: If your rent takes up 40% of your income, you may need to limit your lifestyle spending to 10% or 15% to protect your savings.

- Evaluate your “Needs”: This might involve shopping for cheaper insurance, finding a roommate, or switching to a more fuel-efficient vehicle.

The 20% savings goal should be the last thing you cut. Maintaining this habit is what prevents the cycle of living paycheck to paycheck.

Common Mistakes to Avoid

- Confusing “Wants” with “Needs”: That $100 gym membership might feel like a need, but for budgeting purposes, it is a want. Be honest about what is truly essential.

- Using Gross Income: Always calculate your percentages based on after-tax income. If you use your pre-tax salary, you will significantly overspend.

- Neglecting the Emergency Fund: Many people jump straight to investing before they have a cash safety net. Always fund your emergency savings first.

Professional Tip: Automate Your 20%

The most effective way to ensure you hit your 20% goal is to remove the human element. Set up an automatic transfer from your checking account to your savings or brokerage account on the day you get paid. If the money is moved before you have a chance to see it, you are far less likely to spend it on “Wants.”

Frequently Asked Questions

What if my “Needs” are more than 50% of my income?

If you live in an expensive area, your needs might reach 60% or 70%. In this case, you must subtract the extra percentage from your “Wants” category first. Try to keep your “Savings” as close to 20% as possible.

Does debt repayment count as a “Need” or “Savings”?

Minimum payments on essential debt (like a car or student loan) are considered Needs. However, any extra payments made to principal or paying off high-interest credit cards should be categorized under the 20% Savings/Debt bucket.

Should I count my 401(k) contribution in the 20%?

Yes. If your employer deducts money for retirement before you get your check, that counts toward your 20%. Just make sure you add that amount back to your net pay when calculating your total budget.

Can I use this rule if I have an irregular income?

Yes. Calculate your average monthly income from the previous year. Use that average to set your 50/30/20 targets. In high-income months, put the extra into your savings to cover low-income months.

Is dining out a “Need” if I don’t have time to cook?

No. While everyone needs to eat, the cost of a restaurant meal includes service and convenience, which makes it a Want. Basic groceries are the only food items that fall under Needs.

Practical Takeaway for Success

The 50/30/20 rule is a guideline, not a law. Its primary value is providing a reality check on your spending habits. By categorizing your expenses, you can quickly identify why you might be struggling to save or why your bank account feels empty at the end of the month.

Your next step: Take 15 minutes to look at your bank statements from the last 30 days. Assign every transaction to one of the three buckets and see how close you are to the 50/30/20 target.

Would you like me to help you create a personalized breakdown of these categories based on your specific monthly income?

Sources & Further Reading

For more detailed information on the origin and application of this budgeting method, you can refer to the following authoritative resource:

- Investopedia: The 50/30/20 Budgeting Rule Explained

Disclaimer: The information provided on moneymakeshoney.com is for general informational and educational purposes only and is not intended as professional financial, investment, or tax advice. While we strive for accuracy, we make no representations as to the completeness or reliability of any information provided. Always consult with a qualified financial advisor or tax professional before making any financial decisions.

3 thoughts on “The 50/30/20 Rule: The Simplest Way to Manage Your Budget”