The Great 401(k) Paradox: Why America’s Middle Class is Liquidating Retirement at Record Rates

The U.S. stock market is hitting historic highs, yet a disturbing trend is emerging beneath the surface. While 401(k) balances reach record averages, hardship withdrawals have skyrocketed by 365% since 2021. This analysis examines the systemic fragmentation of the American middle class and the looming “economic disaster” warned by Wall Street’s elite.

The Current Paradox of the American Economy

The paradox is stark: The S&P 500 reached 39 record highs in 2025, pushing the average 401(k) balance to $148,153. However, simultaneously, emergency withdrawals—which incur a 10% penalty and immediate income tax—have surged to unprecedented levels. This divergence signals a profound split in the middle class, where the safety net is being dismantled by necessity rather than choice.

Sources:

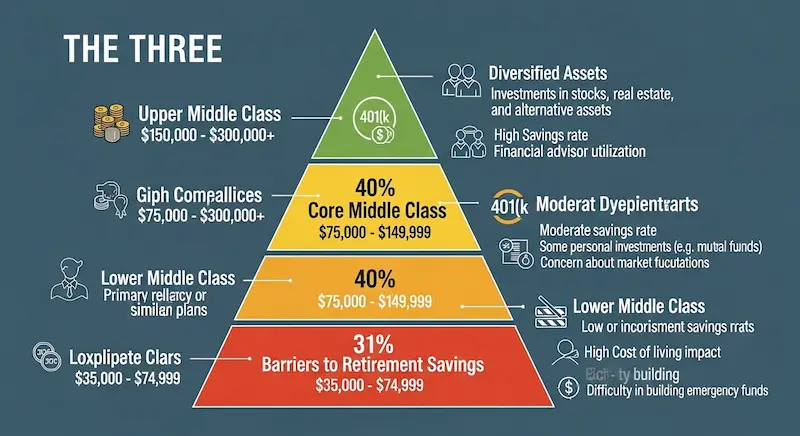

The Fragmented Middle Class: A Tiered Analysis

To understand why Americans are “breaking” their retirement, we must first define who the American middle class is and how their financial health varies by tier.

1. Upper-Tier Middle Class (Top 29%)

- Annual Income: $170,000+

- Asset Portfolio: Diversified across 401(k)s, private brokerage accounts, and real estate

- Resilience: This group drives the “average” 401(k) balance higher, as their participation rate approaches 95%. They benefit directly from stock market rallies.

2. Core Middle Class (40%)

- Annual Income: $56,600 to $170,000 (approximately 52 million households)

- Asset Portfolio: Highly dependent on the 401(k) as their primary or only retirement vehicle

- Current Status: 50% view their 401(k) as their lifeline for retirement, but the median balance is only $38,176—nearly four times lower than the average.

3. Vulnerable Lower Tier (31%)

- Annual Income: Below $56,600

- Barriers: 46% of small businesses do not offer 401(k) plans, leaving 40% of this group with no formal retirement savings mechanism.

Source: Pew Research Center – American Middle Class

Comparative Analysis: Financial Safety Nets vs Market Reality

| Metric | Upper Class / High-Tier | Lower Middle Class / Vulnerable |

|---|---|---|

| Primary Liquidity | Excess Savings & Brokerage | 401(k) Hardship Withdrawals |

| Stock Market Impact | High Growth (S&P 500 Gains) | Indirect/Low (Median $38k) |

| Credit Access | Prime (740+ Credit Score) | Subprime/Limited (<740) |

| Inflation Hedge | Assets (Housing/Stocks) | Wages (Lagging CPI) |

Source: Vanguard – How America Saves 2025

Why the Safety Net is Failing: Three Core Drivers

Expert analysis suggests that the current surge in withdrawals is not a result of poor planning, but a systemic “pincer movement” of inflation and policy changes.

1. The Exhaustion of Pandemic “Excess Savings”

During the pandemic, U.S. households accumulated $2.1 trillion in excess savings due to government stimulus and reduced spending. For the middle class, these reserves were completely depleted by Q1 2023. This marks the exact inflection point where 401(k) withdrawals began to accelerate.

2. The Inflation-Wage Gap and Asset Disparity

While inflation rose 17.8% between 2020 and 2024, wages failed to keep pace. Crucially, upper-tier households saw their stock portfolios grow by over 50%, while the middle class struggled with rising mortgage interest and stagnant real income.

Source: Federal Reserve Economic Data

3. Regulatory Facilitation (SECURE Act 2.0)

Ironically, the government made it easier to tap into retirement funds. The SECURE Act 2.0 allows individuals to withdraw up to $1,000 per year for emergencies without the 10% penalty. While intended to provide flexibility, it has effectively signaled to the public that their retirement is a secondary emergency fund.

Source: IRS – SECURE Act 2.0

Strategic Threat: The “10% Credit Card Interest Cap”

A major volatility factor is the proposed 10% cap on credit card interest rates. While popular in rhetoric, JP Morgan CEO Jamie Dimon has labeled it an “economic disaster.”

If implemented, banks will likely respond by:

- Setting a Credit Floor: Requiring a minimum 740 credit score for all cards

- Credit Contraction: Cutting off nearly 190 million people from revolving credit

- Result: For the 52 million middle-class households with credit scores between 650–750, the loss of credit will force them to liquidate their 401(k)s at an even higher rate

Source: CNBC – Jamie Dimon on Credit Card Cap

People Also Ask (FAQ)

Q: What qualifies as a “Hardship Withdrawal” for a 401(k)? A: Most plans allow withdrawals for “immediate and heavy financial need,” including preventing eviction, paying unreimbursed medical bills, or certain educational expenses.

Q: Why is the median 401(k) balance so much lower than the average? A: High-income earners with six-figure contributions skew the average. The median balance ($38,176) better represents the “typical” American experience.

Q: Is it better to take a 401(k) loan or a hardship withdrawal? A: A loan must be repaid but doesn’t incur the 10% penalty. A withdrawal is permanent and immediately reduces your future compound interest potential.

Q: How does the 10% credit cap affect my retirement? A: If you have a credit score below 740, the cap might lead your bank to close your credit line, forcing you to use retirement savings for short-term emergencies.

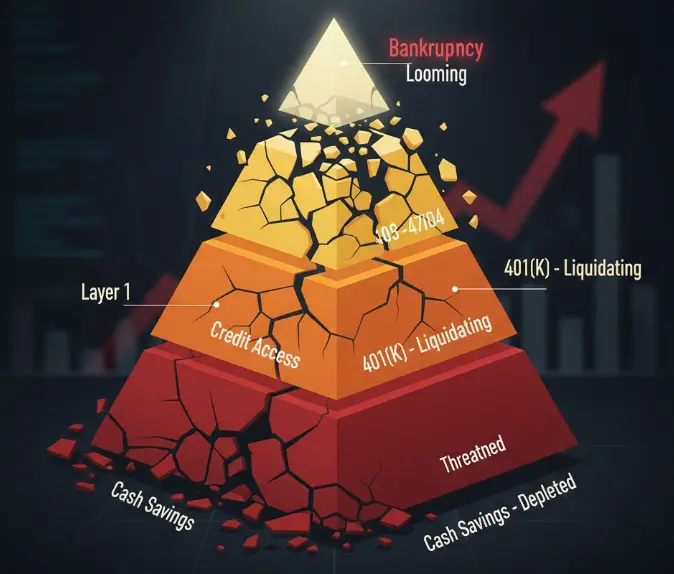

Expert Analysis: A “Four-Layer” Collapse

The American middle class traditionally relied on four layers of security:

- Layer 1: Cash Savings (Depleted in 2023)

- Layer 2: Credit Access (Currently threatened by legislative caps)

- Layer 3: 401(k) Assets (Being liquidated now)

- Layer 4: Bankruptcy (The final stage)

We are currently witnessing the transition from Layer 2 to Layer 3. The record-breaking S&P 500 hides this reality because “Averages Lie.” When the top 29% thrive, the aggregate data masks the fact that 6% of the population is currently burning their future to survive the present.

[401(k)] Verification Checklist

Before you consider tapping into your retirement, verify these four factors:

✓ Alternative Credit: Have you exhausted all low-interest personal loan options?

✓ Tax Impact: Can you afford the 10% penalty plus the addition to your taxable income for the year?

✓ Employer Match: If you withdraw, ensure you are still contributing enough to capture the full employer match (free money).

✓ Hardship Documentation: Do you have the necessary medical or eviction notices to qualify for penalty waivers under SECURE Act 2.0?

Source: IRS – 401(k) Hardship Distributions

Related Resources:

- Federal Reserve – Economic Data

- Pew Research Center – Middle Class Analysis

- Vanguard – Retirement Research

- Fidelity – 401(k) Statistics

Primary Sources:

- U.S. Bureau of Labor Statistics

- Pew Research Center

- Vanguard Group

- Fidelity Investments

- Federal Reserve Economic Data

- Internal Revenue Service (IRS)

Disclaimer: The information provided on moneymakeshoney.com is for general informational and educational purposes only and is not intended as professional financial, investment, or tax advice. While we strive for accuracy, we make no representations as to the completeness or reliability of any information provided. Always consult with a qualified financial advisor or tax professional before making any financial decisions.